The Financial Operating System and Unit Economics: A Strategic Guide to Capital Efficiency

What is the TL;DR?

Direct Answer: A modern Financial Operating System (Financial OS) merges real-time bank ledger data with automated workflows to replace error-prone spreadsheets, reducing invoice processing costs by 79%. In an era of capital efficiency, this real-time visibility is vital for optimizing unit economics (like B2B SaaS target LTV:CAC ratios of 3:1 to 4:1) and proving capital efficiency during intensive 16-to-20-week venture capital due diligence cycles. Startups that achieve positive unit economics early demonstrate a three times better survival rate than their scaling peers.

What is the macroeconomic pathology of startup failure?

Direct Answer: Early and growth-stage startup failure is primarily driven by capital depletion, which serves as the terminal symptom of underlying operational and strategic pathologies. A comprehensive 2024 analysis by CB Insights of 431 failed venture-backed companies revealed that 70% ultimately failed because they ran out of capital. However, the root causes were poor product-market fit (43%), macroeconomic timing (29%), and unsustainable unit economics (19%).

How rapidly does startup capital deplete?

The velocity at which capital is consumed highlights the extreme fragility of the early-stage ecosystem:

- 22 Months to Shutdown: The median time from a company's final fundraise to its ultimate shutdown is just 22 months, during which the average failed startup burns through its remaining runway completely blind.

- $17.5 Billion Destroyed: The 431 failed startups in the 2024 CB Insights cohort had raised a combined $17.5 billion before shutting down, with the median company having raised $11 million.

- 82% Cash Flow Failure Rate: U.S. Bank data indicates that 82% of all business failures are directly attributable to cash flow problems rather than a lack of accounting profitability.

- 74% Premature Scaling Rate: The Startup Genome Project identified that 74% of high-growth internet startups fail due to premature scaling - rapidly draining cash reserves on sales and marketing before securing sustainable unit economics.

- 3x Survival Multiplier: Startups that achieve positive unit economics before their Series B rounds demonstrate a three times better survival rate than their aggressively scaling peers.

How do top-tier VCs recommend managing cash runway?

Top-tier venture capital entities have explicitly warned founders against liquidity mismanagement:

- The Sequoia Capital 12-Month Rule: In their widely circulated "Adapting to Endure" memorandum, Sequoia Capital advised founders to strictly calculate their cash runway, warning that companies with fewer than 12 months of capital face existential threats.

- The Paul Graham "Default Alive" Framework: Y Combinator's founder popularized the framework of calculating whether current cash reserves, combined with current revenue growth and operational expenses, will lead to profitability before running out of capital. Startups that are "default dead" must immediately reduce gross burn or accelerate revenue.

- The Tomasz Tunguz Cash Conversion Cycle (CCC): Tomasz Tunguz (General Partner at Theory Ventures) demonstrates that the speed at which a company converts a dollar of investment into a dollar of cash flow dictates its absolute need for external funding. An efficient company with a 45-day CCC can self-fund growth, whereas a company with a 330-day CCC requires significantly more venture dilution to grow at the same rate.

To address this data disconnect, Y Combinator-backed platforms like Modernbanc are merging real-time bank ledger data with spreadsheet interfaces to prevent the founder overspend that leads to insolvency.

What is the devastating cost of manual financial infrastructure?

Direct Answer: Traditional spreadsheet workflows expose companies to massive operational vulnerabilities, with 88% of all spreadsheets containing errors and 50% of spreadsheet models used by large enterprises harboring material defects (F1F9). Over 70% of companies still rely on manual spreadsheets for budgeting, forecasting, and consolidation, and 73% of companies prepare highly sensitive VAT returns using Microsoft Excel (Deloitte).

What are the error rates and correction costs of manual entry?

The reliance on manual data entry introduces severe cost, time, and accuracy penalties that compound quietly over the fiscal year:

- 1% to 4% Error Rate: According to the Journal of the American Medical Informatics Association, manual data entry carries a baseline error rate of 1% to 4% per field entered. A standard 100-field financial form statistically contains up to four undetected errors.

- 10% Transposition Rate: Transposition errors (e.g., entering $1,350 instead of $1,530) account for approximately 10% of these mistakes.

- 40% Fatigue Penalty: The error rate for manual data entry increases by 40% after four hours of continuous work.

- 95% Undetected Errors: Gartner reports that 95% of data entry errors in the financial services sector go entirely undetected until they cause downstream problems, with each error costing between $53 and $98 to detect, investigate, and correct.

How many hours are lost to inefficient financial workflows?

The labor hours wasted on manual financial administration constitute a massive expense on the corporate P&L:

- 6+ Hours Spent Searching: 50% of finance professionals spend six or more hours per week simply searching for information across disjointed documents, and 13% spend more than ten hours.

- 58% Work About Work: The Asana Anatomy of Work Index found that knowledge workers waste 58% of their time on administrative tasks, including searching for data and chasing approvals.

- 15%+ Spent on AR Collections: In the accounts receivable function, 40% of businesses spend six or more hours per week on manual collections tasks (representing over 15% of a standard 37.5-hour workweek).

What is the annual financial drain of manual operations?

When quantified at the enterprise level, the financial drain is staggering:

- $80,000 to $250,000 Lost: Growing businesses employing between 20 and 100 individuals typically lose between $80,000 and $250,000 annually to hidden manual process costs.

- 79% Processing Cost Reduction: The Institute of Finance & Management (IOFM) reports that the average cost to manually process a single accounts payable invoice is $15.97. An automated financial operating system reduces this cost to $3.24 per invoice—a 79% reduction in overhead.

- 75% to 90% Time Savings: Organizations implementing automation observe a 75% to 90% reduction in overall processing time across the finance function.

How does automation compress the month-end close?

Transitioning from manual spreadsheets to automated financial operating systems drastically compresses the month-end close cycle. Case studies from the expense management platform Ramp highlight this transformation:

- Zola Saved 30 Hours: When the corporate registry Zola migrated from manual spreadsheet expense reporting to an automated system, their finance team saved over 30 hours each month, and their month-end close was compressed from a bloated 20-to-25 days down to just 12-to-13 days.

- 85 Hours Saved Monthly: Another Ramp implementation saved a company 85 hours per month in expense management processes, cutting expense review time from over 6 hours to under 1 hour.

- 73% Time Spent on Analysis: A PwC Finance Effectiveness Benchmark Study indicated that top-quartile finance leaders now spend 73% of their time actively analyzing data rather than collecting it, representing a stark reversal from when 53% of their time was wasted on mundane data gathering.

Operational Metrics: Manual vs. Automated Workflows

| Operational Metric | Manual Spreadsheet / Data Entry Workflows | Automated Financial Operating Systems (API Sync) |

|---|---|---|

| Data Entry Error Rate | 1.0% to 4.0% per field entered | <0.1% to 0.5% with proper API integration |

| Invoice Processing Cost | $15.97 average cost per invoice | $3.24 average cost per invoice (79% reduction) |

| Month-End Close Duration | 8 to 12 days on average (up to 25 days) | 5 to 7 days on average (down to 12 days) |

| AP Processing Time | 15 days on average | 2 to 4 days on average |

| AR Collections Follow-up | 6+ hours weekly for 40% of finance teams | Automated continuous synchronization |

| Hidden Annual Cost (20-100 FTEs) | $80,000 to $250,000 in error correction | Amortized SaaS fees ($10,000 to $60,000) |

How do financial modeling and venture capital fundraising dynamics interact?

Direct Answer: The rigor of a startup's financial modeling and its underlying operational efficiency directly correlate with its ability to successfully raise venture capital. Transitioning from a Seed round to a Series A is statistically the most difficult hurdle in the venture lifecycle; data indicates that only 10% to 15% of seed-funded startups successfully secure a Series A round, with broader industry averages collected by Pitchwise suggesting the overall success rate remains below 40%.

How much time do VCs spend evaluating pitch decks?

Founders consistently and drastically underestimate the scrutiny their financial models face during fundraising:

- 3 Minutes, 44 Seconds: DocSend's behavioral analysis of thousands of pitch decks reveals that investors spend an average of just 3 minutes and 44 seconds reviewing a seed-stage deck. For unsuccessful decks, that review time typical plummets to under two minutes.

- 58% Completion Rate: Only 58% of pitch decks are viewed through to the final slide, meaning nearly half of all investors abandon the narrative before completion.

- High Financial Slide Scrutiny: Within this highly compressed evaluation window, the "Financials" slide receives the second-highest amount of total viewing time, surpassed only by the "Team" slide. VCs use the financials slide to evaluate the founder's grasp of unit economics, burn rate assumptions, and general capital efficiency.

How have market downturns impacted investor attention?

Market downturns have amplified financial scrutiny exponentially:

- 24% Less Overall Attention: Between 2022 and 2023, the overall average time investors spent reviewing pitch decks fell by 24% due to high volume.

- 48% More Scrutiny on Business Models: Investors reallocated their limited attention span, increasing the time spent scrutinizing the business model section by 48% and the traction section by 25%.

- Harsher Filtering: For unsuccessful decks, investors spent 110% more time analyzing weak traction slides and 85% more time trying to decipher flawed business model slides before rejecting the company.

What are the 2026 requirements to secure a Series A?

In 2024 and 2025, venture capital dynamics shifted heavily toward immediate capital efficiency:

- 12-Month Runway Median: Silicon Valley Bank's State of the Markets report highlighted that the median cash runway for tech startups dropped from 16 months in late 2021 to approximately 12 months, forcing nearly 40% of all pre-profit U.S. tech companies to reduce their net burn rates.

- The Burn Multiple: Investors now evaluate the Burn Multiple, which measures how many dollars of cash are burned to generate one dollar of net new Annual Recurring Revenue (ARR). In the artificial intelligence sector, the median Series A company currently burns $5 to gain $1 of new revenue, sparking intense debate over sustainability. Tomasz Tunguz notes that the infrastructure build-out for AI represents a $575 billion bet, where companies are levered 7-to-1 on a cash flow basis to fund data centers.

- 616 Days & $1M-$3M ARR: The average time elapsed between a Seed round and a Series A has stretched to roughly 616 days. During this period, companies must achieve $1 million to $3 million in ARR while demonstrating 15% to 20% month-over-month growth.

- 16 to 20 Weeks Diligence: Due diligence cycles have lengthened from a historical average of 8-to-12 weeks out to 16-to-20 weeks. Startups tracking metrics via manual, error-prone spreadsheets struggle to survive this phase, as unsubstantiated market size claims and disjointed spreadsheets are the primary reasons institutional investors terminate negotiations.

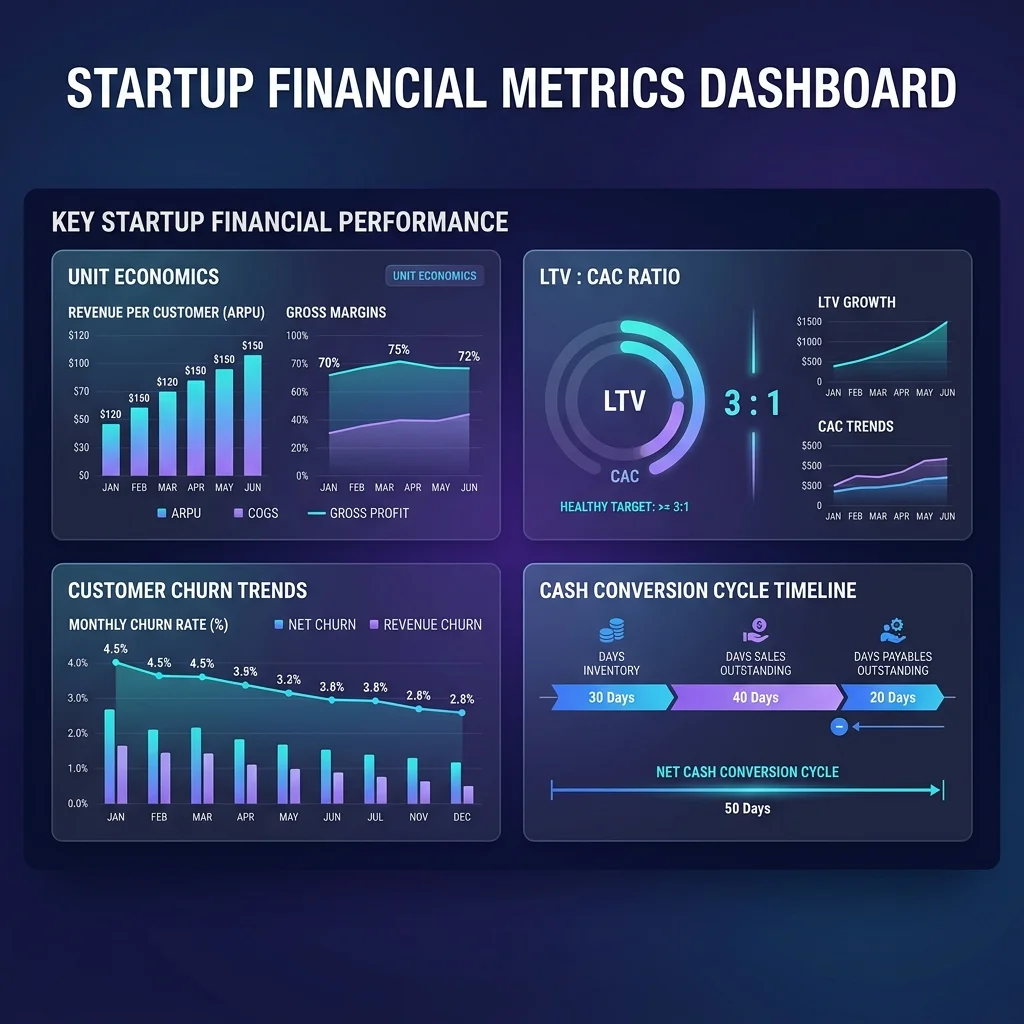

What is unit economics and the LTV:CAC 3:1 standard?

Direct Answer: The mathematical relationship between Customer Lifetime Value (LTV) and Customer Acquisition Cost (CAC) dictates whether a company possesses a sustainable growth engine or a capital incinerator. LTV represents the gross margin profit a customer generates over their entire relationship, while CAC encompasses the fully loaded costs of sales, marketing, tool subscriptions, and onboarding required to secure that customer.

What is the origin of the 3:1 benchmark?

The industry's most widely cited and debated benchmark dictates that a healthy software-as-a-service (SaaS) business should maintain an LTV:CAC ratio of at least 3:1. This ratio implies that for every dollar spent on customer acquisition, the business generates three dollars in gross profit over the customer's lifetime, providing enough margin to cover operational overhead, research and development, and yield net income. This specific "3:1" metric was originally established circa 2010 by David Skok, a General Partner at Matrix Partners, in his seminal "SaaS Metrics 2.0" framework.

What is the "15-Year Drift" of the 3:1 standard?

Modern financial analysts and revenue operators warn against the "15-Year Drift" of this benchmark:

- Steady-State Bias: Skok originally derived the 3:1 rule by observing mature, publicly traded SaaS companies (like Salesforce, HubSpot, and NetSuite) operating at a stable, steady state. The original calculation relied on predictable churn, a realistic multi-year LTV window, and a CAC payback period under 12 months.

- Stage-Specific Adjustments: Early-stage seed companies (under $2 million ARR) typically operate at a 2.5:1 ratio with 120-day payback periods, while growth-stage companies (between $2 million and $10 million ARR) target 3:1 to 4:1 ratios with 90-day paybacks.

- Underinvestment Risk: Demanding a 5:1 or 7:1 ratio too early can signal systemic underinvestment in sales and marketing, indicating to investors that the company is leaving viable, profitable growth on the table.

Why is cash velocity more critical than absolute LTV?

For cash-constrained startups, the CAC payback period is often more critical than the theoretical LTV. For example:

- Scenario A (Slow Velocity): A customer generating a $50,000 LTV but taking 24 months to pay back a $15,000 CAC is objectively worse for immediate cash flow.

- Scenario B (Fast Velocity): A $30,000 LTV customer who pays back their $6,000 CAC in just 8 months is better for immediate cash flow.

The faster velocity of capital in Scenario B allows the firm to reinvest the recouped cash multiple times within the same fiscal year, compounding growth without drawing down venture reserves.

Why is customer retention and reducing churn critical?

Direct Answer: Customer retention is the most powerful mathematical lever for optimizing unit economics, as reducing churn extends the lifetime of the customer and geometrically compounds their total value. A classic analysis by Fred Reichheld at Bain & Company established that a mere 5% increase in customer retention produces an outsized 25% to 95% increase in total corporate profitability.

Why do repeat customers provide superior margins?

This disproportionate return occurs because retained customers progressively cost less to serve, expand their usage over time, and act as referral mechanisms that organically lower the aggregate CAC:

- 9x More Likely to Convert: Research from Harvard Business School and Adobe indicates that repeat customers are 9 times more likely to convert on secondary offerings than first-time shoppers.

- 46% Annual Revenue Loss: Customer churn has a compounding effect on SaaS cash flow. As financial modeling platform Trezy highlights, a 5% monthly churn rate does not equate to a 60% annual loss; because it compounds, a 5% monthly churn rate means the company loses 46% of its starting revenue base annually. Every churned customer permanently reduces future cash flow, forcing the company to spend increasingly expensive acquisition dollars just to maintain a flat revenue trajectory.

- $2.00 to Acquire $1.00 of ARR: In 2026, B2B SaaS customer replacement costs are higher than ever. The average B2B SaaS company now spends $2.00 to acquire $1.00 of new ARR, a cost that has risen 14% since 2023 due to increased advertising costs, zero-click search behavior, and broad market saturation.

What are the 2026 unit economics benchmarks across industries?

Direct Answer: Unit economics benchmarks vary drastically across different business models and sectors. Evaluating an enterprise SaaS company against direct-to-consumer (DTC) metrics is fundamentally flawed. Below is a detailed tabular comparison of 2026 baseline expectations for scaling companies, segmented by industry and acquisition model.

2026 Unit Economics Industry Benchmarks

| Industry / Segment | Average CAC Range | Average LTV Range | Target LTV:CAC Ratio | Typical CAC Payback |

|---|---|---|---|---|

| B2B SaaS (Enterprise) | $5,000 to $250,000+ | $300,000 to $1,000,000+ | 3.2:1 to 5:1+ | 18 to 36 months |

| B2B SaaS (Mid-Market) | $1,200 to $2,000 | $80,000 to $200,000 | 3.2:1 to 4:1 | 14 to 18 months |

| B2B SaaS (SMB) | $200 to $700 | $15,000 to $40,000 | 2.5:1 to 3:1 | 6 to 12 months |

| FinTech (Consumer) | $1,340 to $2,140 | Variable by product mix | 4:1 to 5:1 | 6 to 18 months |

| eCommerce (DTC) | $68 to $156 | Variable by AOV/frequency | 1.5:1 to 3:1 | 1 to 3 months |

| Healthcare (Digital-First) | $742 to $3,870 | Highly variable | 3:1 | 6 to 24 months |

How do metrics differ between Enterprise SaaS, PLG, and FinTech?

The underlying dynamics of each sector dictate these benchmarks:

- B2B Enterprise SaaS: Sales cycles span 6 to 12 months, requiring multi-threaded sales processes, intensive security reviews, and executive sponsorship. Consequently, enterprise CAC routinely exceeds $10,000, which is acceptable given that the resulting LTV often scales beyond $300,000 due to multi-year commitments and net revenue retention rates that surpass 120%.

- Product-Led Growth (PLG): PLG models rely on self-serve funnels, compressing CAC to a highly efficient $100 to $500 range, allowing companies to recover acquisition costs within a rapid 2 to 6 months.

- FinTech: The FinTech sector faces unique headwinds due to regulatory complexities and fierce competition for consumer attention. Consumer FinTech applications observe steep acquisition costs ranging from $1,340 to $2,140. Due to these high upfront costs, FinTech investors now demand rigorous LTV:CAC ratios of 4:1 to 5:1. Meanwhile, B2B FinTech SaaS exhibits an average CAC of $1,450, a figure that is actively trending upward by over 15.3% year-over-year.

- eCommerce & DTC: eCommerce brands experience much lower nominal acquisition costs ($68 to $156). However, because individual transaction values are lower, the LTV:CAC threshold is much tighter, hovering between 1.5:1 and 3:1. Subscription-based DTC models can achieve an incredibly efficient effective CAC of $17.67 per month, driving payback periods down to 1 to 2 months.

- Healthtech: Healthtech bridges the gap between consumer and enterprise mechanics, with digital-first patient acquisition costing roughly $742, whereas B2B hospital system sales skyrocket to an average CAC of $3,870.

How does strategic integration build startup capital efficiency?

Direct Answer: Transitioning to automated financial operating systems yields second-order benefits extending far beyond the 79% reduction in invoice processing costs. Real-time API synchronization enables immediate calculation of the Cash Conversion Cycle, empowering executives to compress the latency between accounts payable and accounts receivable and fund growth without premature venture dilution.

What advantages does an automated Financial OS offer in due diligence?

Possessing an auditable, automated financial ledger provides a distinct, quantifiable competitive advantage:

- Prevents Downstream Spreadsheet Errors: By replacing error-prone spreadsheets (which carry an 88% baseline error probability) with automated financial systems, companies prevent the downstream propagation of errors, which traditional manual double-data entry methods can only reduce to 0.5% while doubling human labor costs.

- Calibrates Stage-Appropriate Benchmarks: Founders can dynamically monitor their LTV:CAC metrics to avoid underinvesting in their growth engine (e.g., leaving cash unspent at a 7:1 ratio) or scaling an unsustainable business model (e.g., masking a 1:1 ratio with vanity metrics).

- Protects Retention-Driven Profit Expansion: Reallocating capital away from top-of-funnel acquisition and investing in product onboarding and customer success structurally protects the baseline revenue that guarantees a "default alive" trajectory.

In a fundraising environment where due diligence spans 16 to 20 weeks and investors ruthlessly scrutinize burn multiples, a granular, real-time command of cash flow is the mandatory baseline for survival.